Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

The Philippines has 37 million unbanked adults — yet loan app usage surged from 47 million to 67 million users between 2023 and 2024. That gap between the unbanked and the digitally connected is exactly where lending apps operate, filling a real need that traditional banks have long ignored.

But the same speed and accessibility that makes these apps useful has also attracted predatory operators. In just April and May 2025, the Presidential Anti-Organized Crime Commission (PAOCC) received more than 13,000 complaints involving online lending apps — harassment, threats, data theft, and fake court orders.

This guide helps you find the right app for your situation, verify it’s legitimate, and borrow without putting your data or finances at risk.

| Feature | What to Know |

| ⚡ Fastest approval | 3–5 minutes (JuanHand, Digido, Mocasa) |

| 💰 Loan range | ₱1,000 – ₱125,000 (depending on app & profile) |

| 📋 Minimum requirement | 1 valid government-issued ID + active mobile number |

| 🎁 First loan at 0% interest | Yes — Digido (0% for 7 days), JuanHand (select users) |

| 🔍 Must verify | SEC registration at sec.gov.ph before applying |

| ⚠️ Scam complaints | 13,000+ filed with PAOCC in just April–May 2025 |

Before downloading anything, identify which borrower profile matches you. Each situation calls for a different app — picking the wrong one wastes time and can cost you more than necessary.

Check the Borrow tab in your GCash app first. If you have a GLoan offer, that’s your cheapest option at 1.59% per month — far lower than most lending apps. If no offer appears, see Section 4 on how to build your GScore to unlock it.

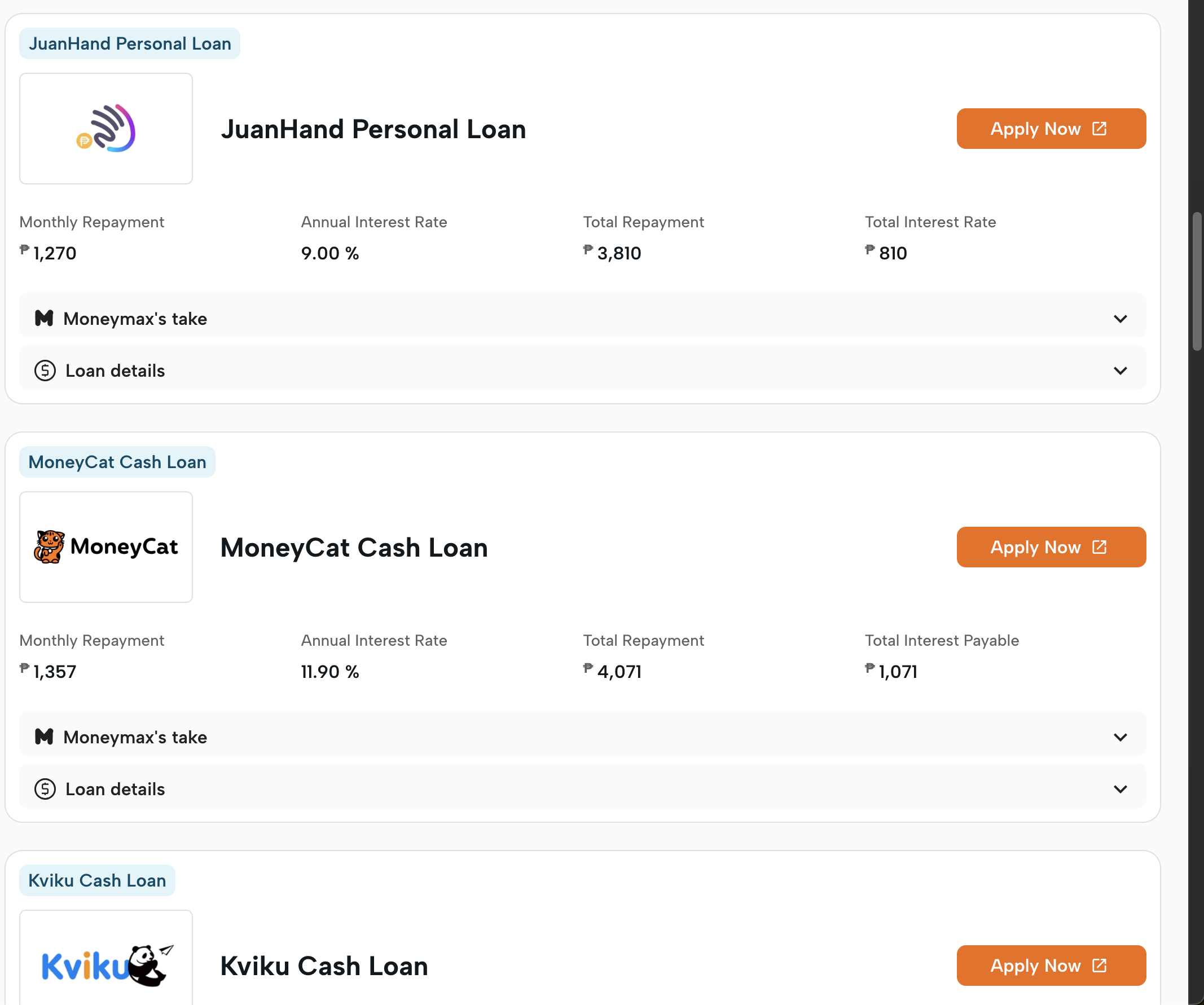

JuanHand and Digido both approve in 5 minutes with just one valid ID. Digido’s acceptance rate is 90–95%, making it one of the most accessible. If this is your first time borrowing, Digido’s 0% interest on the first loan (up to ₱4,000, for 7 days) is hard to beat.

Good news: Tala, JuanHand, and Mocasa explicitly accept borrowers without payslips. These apps use alternative credit scoring — your e-wallet transaction history, digital footprint, and basic personal information — instead of requiring employment papers. Bank statements showing consistent income also help, but are not always required.

Finbro is your best bet for larger amounts among fintech apps, offering up to ₱50,000 for repeat borrowers and 0% interest for the first 7 days. For truly large sums with the lowest possible rates, a traditional bank personal loan remains the gold standard — though you’ll need payslips, ITR, and a credit history.

Digido offers the first ₱4,000 at 0% interest to new borrowers. Finbro offers 0% for the first 7 days on amounts up to ₱15,000 for new users. JuanHand also runs occasional 0% promos for first-time borrowers. Always read the fine print — the 0% applies only if you repay within the specified window.

| → Compare verified loan apps for your profile: [AFFILIATE LINK] |

All apps in this table are SEC-registered. Interest rates and terms are based on publicly available information as of June 2026 and may change.

| App | Max Loan | Interest Rate | First Loan | No Payslip? | Approval |

| GCash GLoan | ₱125,000 | 1.59%/month | Invite-only | ✅ | Instant* |

| JuanHand | ₱50,000 | 0.025%/day | ₱2K–₱5K | ✅ | 5 min |

| Tala | ₱15K / ₱60K (Maya) | ~15%/month flat | ₱1K–₱3K | ✅ | Minutes |

| Digido | ₱25,000 (repeat) | Varies | ₱4K at 0% | ✅ | 5 min |

| Finbro | ₱50,000 (repeat) | 0.2%/day | 0% for 7 days | Mostly | 24 hrs |

| Mocasa | ₱50,000 | 0.2%/day | – | ✅ | 5 min |

| Bank Personal Loan | Up to ₱2M+ | Lowest APR | By application | ❌ | 3–7 days |

| * GLoan is invite-only — it cannot be applied for on demand. You must qualify through your GScore and GCash activity history. See Section 4 for how to unlock it. |

| → See current rates and apply through verified links: [AFFILIATE LINK] |

GLoan — GCash’s personal loan product powered by Fuse Financing, Inc. — offers the lowest interest rate among all major loan apps in the Philippines, as low as 1.59% per month. But there’s a catch most guides don’t explain clearly: you cannot apply for GLoan whenever you want.

GLoan is an invitation-only product. GCash evaluates your eligibility weekly using an automated scoring system called GScore. If you qualify, the offer appears in your Borrow tab — and if it doesn’t appear, no amount of contacting GCash support can change that. No third-party agent can “unlock” your GLoan access either. Anyone claiming otherwise is running a scam.

GScore is calculated based on your actual behavior inside the GCash ecosystem. Here’s what moves the needle:

| GCash Behavior | Why It Helps Your GScore |

| Pay bills via GCash | Meralco, PLDT, water, internet — each payment = positive signal |

| Use GSave regularly | Maintain a minimum ₱500 balance and top up consistently |

| Keep GCredit in good standing | Highest single impact: on-time GCredit payments signal creditworthiness |

| Use GCash for QR purchases | Frequent in-store or online purchases improve activity score |

| Complete your profile | Full name, verified number, address — incomplete profiles lower chances |

| Keep your account active | Dormant accounts rarely qualify — log in and transact weekly |

| 💡 Real case: A borrower from Bulacan shared in a Filipino finance group that his GScore rose from 380 to 492 in six months — just by consistently paying his Meralco and internet bills via GCash and keeping a ₱500 minimum in GSave. That was enough to unlock his first GLoan offer of ₱10,000. |

If you don’t have a GLoan invitation yet, don’t wait — these alternatives approve anyone who meets basic requirements:

| → No GLoan invite? These apps accept your application today: [AFFILIATE LINK] |

Being available on the Play Store or App Store does not mean an app is legal. In early 2025, the SEC found 22 unregistered lending apps still active on Google Play — all violating SEC Memorandum Circular 10. Here’s how to verify before you apply.

Scam apps routinely copy names of legitimate lenders. The app name “FastPeso” means nothing. You need the actual corporate name, which is usually found in the app’s About page, Terms of Service, or Play Store description. Look for something like: “Operated by XYZ Lending Corporation.”

Go to sec.gov.ph → navigate to the list of recorded online lending platforms. Search the corporate name. The company must appear here AND have a valid Certificate of Authority (CA) to operate as a lending company — not just a basic SEC incorporation.

A legitimate app will display its SEC Registration Number and Certificate of Authority number in its own materials. Cross-reference what the app shows against what’s in the SEC database. If they don’t match, walk away.

Under this 2025 rule, all licensed lenders must show the full APR, all fees, and the total repayment amount before you confirm the loan. If you’re being rushed to accept without seeing these numbers — that’s a violation and a warning sign.

| → Only browse apps that have been pre-verified for SEC registration: [AFFILIATE LINK] |

| → Start your application with a verified, SEC-registered lender: [AFFILIATE LINK] |

Online lending fraud complaints filed with the PAOCC reached 13,000 in just two months (April–May 2025). The SEC has shut down dozens of apps, but new ones appear constantly. Watch for these five warning signs:

| 🚩 1 | Charges a fee BEFORE releasing funds | No legitimate lender ever asks for a “processing fee,” “insurance,” or “activation fee” upfront. If they do — it’s a scam. Legit apps always deduct fees from the loan proceeds after approval. |

| 🚩 2 | Requests access to your contacts or gallery | A real loan app never needs your contact list or photos to process a loan. Apps that ask for this permission use it to harass borrowers and publicly shame them or their friends and family. |

| 🚩 3 | Not on SEC’s recorded online lending platforms list | Check sec.gov.ph for the official list. Being on the Play Store does NOT equal being SEC-registered — many illegal apps passed store review using fake descriptions. |

| 🚩 4 | Promises “guaranteed approval” | All legitimate lenders perform KYC (Know Your Customer) checks. “Guaranteed approval” is a red flag — it means they skip verification and are likely preparing to trap you with predatory terms. |

| 🚩 5 | Sends fake court orders or legal threats | Starting in 2025, scam apps began using forged Regional Trial Court documents and fake judges’ names. The Supreme Court itself issued a public warning. Real courts never contact you through a lending app. |

| 📞 Where to report: SEC → flcd_queries@sec.gov.ph | NPC (data privacy) → privacy.gov.ph | CICC Hotline: 1326 | PAOCC → paocc.gov.ph |

It depends on the app and your receiving account. E-wallet disbursement (GCash, Maya, ShopeePay) typically arrives within minutes after approval. Bank transfers via InstaPay usually take 1–2 hours. Applying on weekday business hours gives you the fastest results — some banks have cutoffs for same-day processing.

Yes. Apps like JuanHand, Tala, Digido, and Mocasa do not require payslips. They use alternative scoring based on your digital transaction history, ID verification, and basic personal information. If you receive payments through GCash or Maya regularly, that history can serve as your proof of income with GCash’s GLoan or Maya Credit.

“Tapal-tapal” is Filipino slang for the practice of borrowing from one loan app to pay another — essentially using debt to cover debt. It was identified in a 2025 investigation as the most common debt spiral among Filipino online borrowers. Short loan terms (7–14 days) and high rates make this trap especially easy to fall into. If you find yourself doing this, stop taking new loans and contact each lender to request a payment extension before the due date.

Yes. Most modern loan apps support disbursement to GCash, Maya, or other e-wallets. You can then cash out at 7-Eleven, Cebuana Lhuillier, or GCash partner outlets. Some apps also offer cash pickup at partner payment centers. A bank account is helpful but no longer mandatory for smaller loans.

Late fees are charged immediately, and the lender reports the delinquency to the Credit Information Corporation (CIC). This affects your credit score and can reduce future borrowing limits. Legitimate apps like JuanHand, Tala, and Finbro have extension options — contact the app’s customer service before the due date if you know you’ll be late. Do not ignore overdue notices hoping they go away; this only makes the debt grow.

| → Compare your best options and borrow responsibly today: [AFFILIATE LINK] |

Loan apps in the Philippines offer genuine financial inclusion for millions who have no access to traditional banking — but the same urgency that drives people to download them is exactly what illegal operators exploit.

Before you apply anywhere, remember three things:

| → Find the right verified loan app for your profile: [AFFILIATE LINK] |

Data note

Interest rates, loan limits, and app features are based on publicly available information from official app stores, lender websites, and Philippine government sources as of June 2026. Figures may change at lender discretion. This article is for informational purposes only and does not constitute financial advice. Always review the full loan terms before signing. Replace [AFFILIATE LINK] with your verified partner links before publishing.